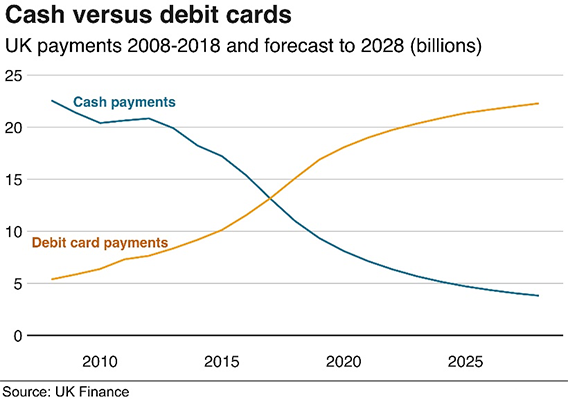

Ben Calvert: Debt Collection relies heavily on digital payment methods due to the prevailing trend of cashless transactions in today's society. Over the past decade, there has been a significant shift away from cash. With UK Finance projecting that cash will constitute less than 5 percent of transactions by 2025, compared to nearly 25 percent a decade ago.

This transformation is closely tied to the emergence of new digital payment methods facilitated by digital wallets, initially pioneered by PayPal and further popularised by services like GPay and ApplePay. Leveraging the widespread use of smartphones, these technologies have effectively replaced physical wallets and transformed the landscape of financial transactions.

Even traditional payment methods, such as Standing Orders, have experienced a modern resurgence through innovations like Open Banking. This allows for seamless connectivity through smartphone banking apps, eliminating the need for cumbersome paperwork and traditional forms of transaction initiation.

For collections agencies, understanding and adapting to this digital payment landscape is crucial. As these agencies intervene in people's lives when they require a quick, frictionless, and stress-free approach to managing debt, offering customers the ability to pay on their terms using the most convenient methods is essential.

Just as intrusive engagement methods can deter customers, a complicated transaction process is equally off-putting. Therefore, embracing digital payments aligns with customer preferences, providing a familiar and efficient avenue for debt settlement.

This transformation is closely tied to the emergence of new digital payment methods facilitated by digital wallets, initially pioneered by PayPal and further popularised by services like GPay and ApplePay. Leveraging the widespread use of smartphones, these technologies have effectively replaced physical wallets and transformed the landscape of financial transactions.

Even traditional payment methods, such as Standing Orders, have experienced a modern resurgence through innovations like Open Banking. This allows for seamless connectivity through smartphone banking apps, eliminating the need for cumbersome paperwork and traditional forms of transaction initiation.

For collections agencies, understanding and adapting to this digital payment landscape is crucial. As these agencies intervene in people's lives when they require a quick, frictionless, and stress-free approach to managing debt, offering customers the ability to pay on their terms using the most convenient methods is essential.

Just as intrusive engagement methods can deter customers, a complicated transaction process is equally off-putting. Therefore, embracing digital payments aligns with customer preferences, providing a familiar and efficient avenue for debt settlement.